Choosing between term life insurance and whole life insurance is one of the most common—and important—decisions Canadians face when securing financial protection. While both provide a crucial safety net for your loved ones, they are designed for different needs and goals.

This guide breaks down the key differences to help you make an informed choice on term vs whole life insurance, whether you’re in Brampton, the GTA, or beyond.

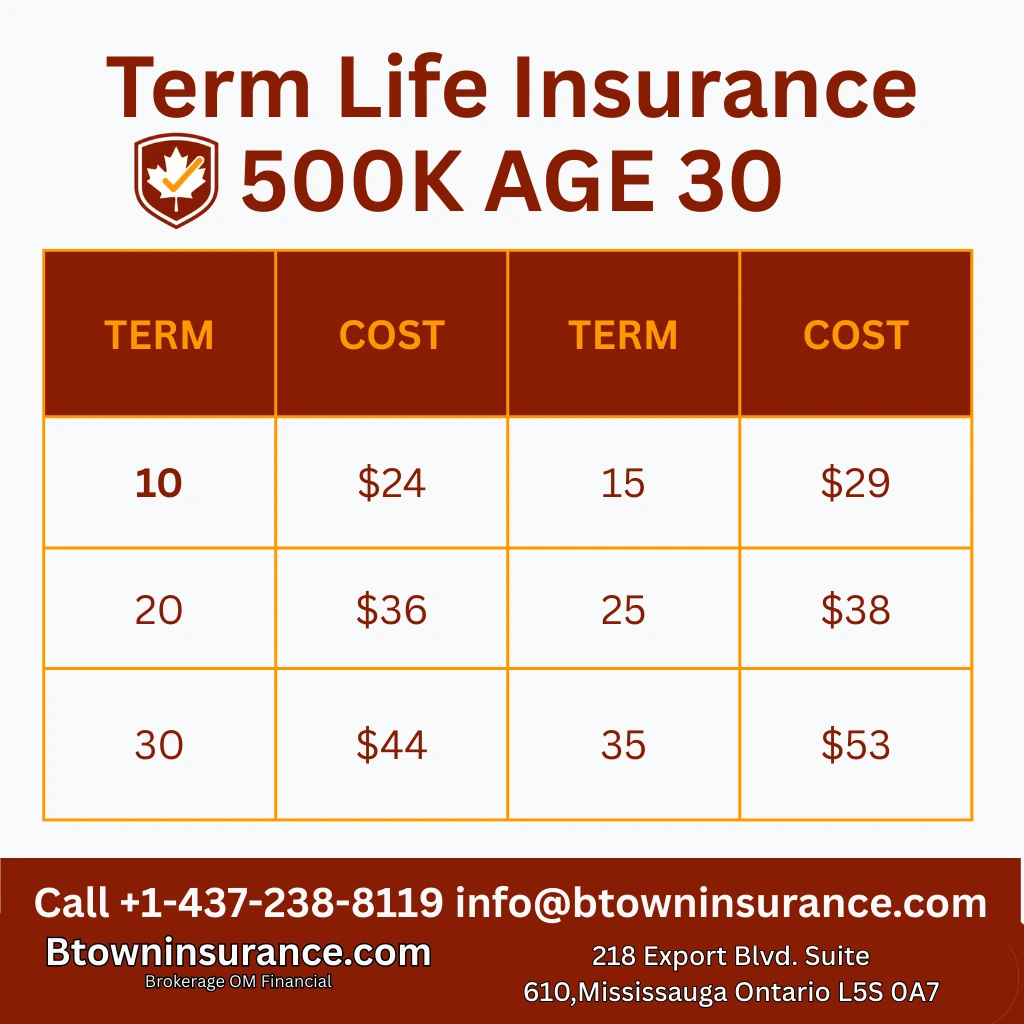

What Is Term Life Insurance?

Term life insurance is straightforward protection for a specific period, such as 10, 20, or 30 years. If the policyholder passes away during the term, the insurance company pays a tax-free death benefit to the chosen beneficiaries. It’s pure protection with no investment component.

Key Features of Term Life Insurance

- Affordable Premiums: Significantly lower cost for a higher amount of coverage.

- Fixed Term: Coverage lasts for a predefined period (e.g., until your mortgage is paid or children are independent).

- No Cash Value: It is solely a death benefit policy with no savings or investment element.

- Simplicity: Easy to understand and compare.

Who Should Choose Term Life Insurance?

Term life is often the best fit for:

- Young Families: Needing maximum coverage on a budget.

- Homeowners with a Mortgage: To ensure the mortgage can be paid off.

- Parents with Dependent Children: To replace income and fund future needs like education.

- Those with Temporary Debt: Covering business loans or other time-limited obligations.

For most families in Ontario, term insurance provides the essential, high-coverage protection they need at an affordable price.

What Is Whole Life Insurance?

Whole life insurance is a form of permanent life insurance that provides lifelong coverage. Beyond the guaranteed death benefit, it includes a savings component known as “cash value,” which grows at a guaranteed rate over time and can be accessed during your lifetime.

Key Features of Whole Life Insurance

- Lifetime Coverage: Protection that lasts your entire life, as long as premiums are paid.

- Guaranteed Cash Value: A savings element that grows tax-deferred and can be borrowed against or withdrawn.

- Level Premiums: Premiums are fixed and guaranteed not to increase.

- Estate Planning Tool: Can provide tax-efficient wealth transfer to beneficiaries.

Who Should Choose Whole Life Insurance?

Whole life insurance may be suitable for:

- High-Income Individuals seeking tax-advantaged savings.

- Business Owners for buy-sell agreements or key person insurance.

- Those with Complex Estate Planning Needs to cover final taxes or leave a legacy.

- Individuals who want forced savings with a conservative, guaranteed return.

Term vs Whole life insurance table

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Coverage Length | Temporary (10, 20, 30 years) | Permanent (Lifetime) |

| Premiums | Lower (initially) | Higher (but fixed) |

| Cash Value | No | Yes (Guaranteed growth) |

| Primary Purpose | Income replacement, debt coverage | Estate planning, wealth transfer, lifelong protection |

| Flexibility | Can often convert to permanent | Fixed benefits, but with loan options |

Which is better?, Term vs Whole life Insurance

There’s no universal “better” option. The right choice is a personal decision based on:

- Your Budget: How much can you comfortably allocate to premiums?

- Your Stage of Life: Are you covering temporary needs or planning for lifelong goals?

- Your Financial Objectives: Is your goal pure protection, or do you want a savings component?

- Your Health & Age: These directly affect eligibility and cost.

A popular strategy is to combine both: use term insurance to cover major, time-sensitive obligations (like a mortgage or raising children), and add a whole life policy for permanent needs and estate planning.

For example, many families in Brampton and the GTA start with term life to:

- Protect their family home by covering the mortgage.

- Replace lost income to maintain their family’s standard of living.

- Secure their children’s future by funding education costs.

Why Work With a Licensed Life Insurance Broker?

Navigating insurance options alone can be confusing. An independent broker works for you, not one insurance company. A broker provides:

- Objective Comparisons: Access to multiple top insurers to find the best rates and features.

- Expert Guidance: Clear explanations to help you understand the fine print.

- Cost Savings: Finding the right policy structure to avoid overpaying.

- Ongoing Service: Support with claims, changes, and reviews over time.

Working with a local Brampton life insurance broker means getting personalized advice that understands your community’s unique needs.

Get a Free, No-Obligation Life Insurance Quote

Deciding between term vs whole life insurance is a significant step. Professional guidance can ensure you get the right coverage at the best value, giving you peace of mind for the future.

📞 Call or Text: 437-238-8119

🌐 Visit: btowninsurance.com

Still have questions on term vs whole life insurance? Free Consultation • No Pressure • Serving Ontario, Alberta, and BC

Leave a Reply